A booking comes in, the client pays the deposit, you reserve the day — and weeks later your payment processor claws the money straight back out of your account, often with a fee on top. You delivered the session, but you’re now out both the time and the cash. This is the recording studio chargeback scam, and because it abuses a system designed to protect honest customers, it can catch even careful studios. Here’s how it works and how to make your bookings chargeback-proof.

How the recording studio chargeback scam works

A chargeback is a legitimate consumer protection: a cardholder disputes a charge and the bank reverses it. Fraudsters exploit that process deliberately. The scam usually runs like this:

- The booking and deposit. A client books studio time and pays by card — a deposit or the full amount. Everything looks normal.

- The session goes ahead. You hold the date, do the work, and deliver the recording, mix or masters.

- The dispute. Sometime later, the cardholder tells their bank they didn’t authorise the charge, or claims the service was “never provided” or “not as described.”

- The reversal. The bank pulls the funds back from you while it investigates, and your processor typically adds a chargeback fee. Without solid evidence, the money often stays gone.

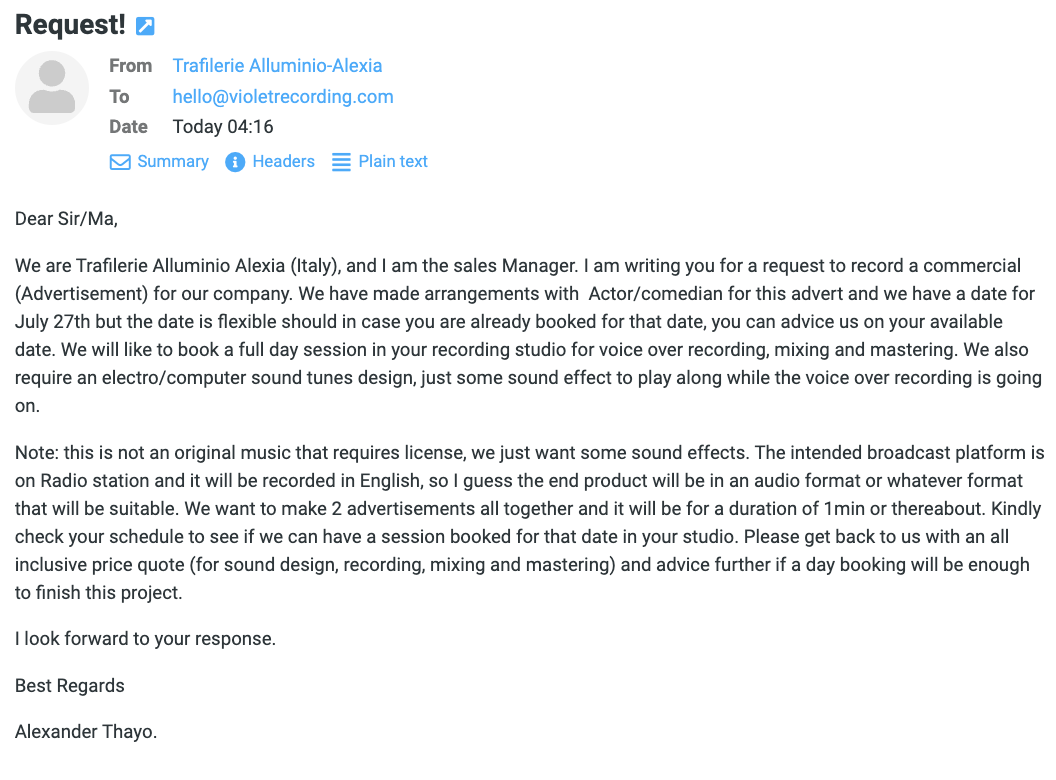

There are two flavours. “Friendly fraud” is a real client with buyer’s remorse who disputes a charge they recognise — sometimes after getting exactly what they paid for. True fraud uses a stolen card, where the real cardholder later, rightly, disputes it; this often overlaps with the overpayment pattern in our “record our commercial” scam email breakdown.

Why studios are exposed to chargebacks

A few things about studio work make chargebacks especially awkward to fight:

- The product is intangible. Unlike a shipped item with a tracking number, “studio time” or a digital mix has no parcel to prove delivery — so “I never received it” is harder to refute.

- Card-not-present is normal. Remote clients pay online without a physical card or signature, which is exactly the transaction type with the weakest fraud protection for the merchant.

- Bespoke, higher-value invoices. Sessions cost real money, so a single successful dispute hurts — and makes you a worthwhile target.

- Informal paperwork. Many studios book on a friendly email and a verbal yes, leaving little documentation to win a dispute.

None of this means card payments are a trap — they’re convenient and clients expect them. It just means the protection has to come from your process, not your processor.

The red flags before a chargeback

Some bookings carry warning signs worth a second look:

- Mismatched details. A cardholder name, email and billing country that don’t line up with the person you’re actually dealing with.

- Rushed, high-value first bookings. A brand-new client wanting a large session immediately, paid in full by card, with no interest in a call or a contract.

- Reluctance to sign anything. Pushback on a simple booking agreement or deposit terms.

- Pressure to refund off-card. Asking for a cancellation refund by bank transfer or another method than the original card is a known money-laundering and stolen-card tell.

- Overpayment. The same signature move as other studio scams — paying more than invoiced, then requesting the difference back.

How to protect your studio from chargebacks

You can’t stop a client from filing a dispute, but you can make sure the evidence is overwhelmingly on your side — which is what wins them:

- Use a written booking agreement. Clear terms covering the service, the date, deposits, cancellation and that work is bespoke and non-refundable once started. A signed agreement is your strongest evidence.

- Keep a paper trail. Save the booking emails, the brief, file-delivery confirmations and any sign-off. Documented proof of delivery is the single best defence in a dispute.

- Take deposits and confirm cleared funds. Non-refundable deposits deter casual disputes; only commit the date once the payment has genuinely cleared.

- Always refund to the original card. Never refund a card payment by transfer or cash — that pattern is exactly how stolen-card fraud is laundered.

- Use a reputable processor and respond fast. Good payment providers give you a window to submit evidence; reply promptly with your agreement and delivery proof.

One detail that catches studios out: with cards and cheques, your bank may show the money as available within a day or two, but that is not the same as it being settled beyond reversal. Treat large incoming payments as provisional until you’re sure they’ve truly cleared.

Common mistakes that lead to lost disputes

Studios rarely lose chargebacks through anything reckless — usually it’s missing paperwork:

- No written agreement. Without documented terms, “not as described” is very hard to argue against.

- No proof of delivery. If you can’t show the files were sent and received, the “never provided” claim sticks.

- Refunding off the original card. The most expensive cancellation mistake, and a laundering red flag.

- Ignoring the processor’s evidence deadline. Disputes have tight response windows; miss it and you forfeit automatically.

- Treating available funds as final. Acting on a payment before it has truly settled.

What to do if you get hit with a chargeback

Respond within your processor’s deadline and submit everything you have: the signed agreement, booking correspondence, the brief, and proof you delivered the work. If it involved a stolen card or a clearly fraudulent dispute, report it to your national fraud authority such as the FBI’s Internet Crime Complaint Center (IC3). To recognise the upstream version that often precedes a reversal, read our guide to the voice over booking scam.

Frequently asked questions

What is a chargeback scam?

It’s when someone abuses the card-dispute system to reverse a legitimate payment — either a real client falsely claiming a service wasn’t provided (“friendly fraud”), or a fraudster using a stolen card that the true owner later disputes.

Can I win a chargeback dispute as a studio?

Often yes, if you have evidence. A signed booking agreement, the brief, and proof you delivered the files give you a strong case. Disputes are usually lost when there’s no paperwork to submit.

Should I stop taking card payments to avoid chargebacks?

No — clients expect cards and they’re convenient. The protection comes from your process: written terms, deposits, proof of delivery, and only ever refunding to the original card.

A client wants a refund to a different account than they paid from. Is that okay?

Treat it as a serious red flag. Always refund to the original payment method. A request to refund elsewhere is a known sign of stolen-card fraud and money laundering.